The Securities and Exchange Act B.E. 2535, amended version, effective on August 31, 2008 (Section 89/12), prescribed the Securities and Exchange Commission (SEC) to lay out details and oversee connected transactions of the listed companies. Therefore, SEC issued SEC Announcement Tor.Jor.21/2551 on connected transaction rules for the listed companies, dated 31 August 2008, to abide by.

Presently, the SEC has revised the aforementioned regulations to ensure greater clarity, align with current circumstances, and elevate the protection of investors' rights. Consequently,the Capital Market Supervisory Board has issued Notification No. TorChor. 46/2568 Re: Rules on Related Party Transactions, which is scheduled to come into effect from 1 July 2026 onwards.

Presently, the SEC has revised the aforementioned regulations to ensure greater clarity, align with current circumstances, and elevate the protection of investors' rights. Consequently,the Capital Market Supervisory Board has issued Notification No. TorChor. 46/2568 Re: Rules on Related Party Transactions, which is scheduled to come into effect from 1 July 2026 onwards.

Rules Summary |

Related Party Transaction means a transaction between a listed company or its subsidiary and an individual or a juristic person whose relationship qualifies them as a related party of the listed company. This may give rise to concerns regarding conflicts of interest. Therefore, it is necessary to establish regulatory rules to ensure that entering into such transactions is conducted with transparency and fairness, and with the utmost regard for the best interests of the listed company and its shareholders. In this connection, the listed company is duty-bound to disclose information to the shareholders, as well as to provide opportunities for the shareholders to participate in the consideration and decision-making process regarding the entry into such transactions.

*Applicable only to companies listed on the SET/mai (excluding LiVEx), and also includes companies whose common shares have been delisted but which still have obligations to prepare and submit reports on financial position and operating results under Section 56 of the Securities and Exchange Act.

*Applicable only to companies listed on the SET/mai (excluding LiVEx), and also includes companies whose common shares have been delisted but which still have obligations to prepare and submit reports on financial position and operating results under Section 56 of the Securities and Exchange Act.

Definition |

Subsidiary means a limited company or a public limited company under the control of a listed company in any of the following manners (including chain-principle structures down through all tiers) as follows:

- - Holding voting shares exceeding 50% of the total voting rights.

- - Having direct or indirect control over the majority of voting scores in the shareholders' meeting of such juristic person, or by any other reasons.

- - Having direct or indirect control over the appointment or removal of directors from one-half of the total number of directors onwards.

Transactions Subject to the Rules Governing Related Party Transactions (RPT)

Entering into or agreeing to enter into any contract or agreement with a related party, whether directly or indirectly, which gives rise to the following transactions, including the creation of rights or the waiver of rights to engage in such actions::

- - Acquisition or disposal of assets

- - Lease or rental of assets

- - Provision or receipt of services

- - Provision or receipt of financial assistance

- - Issuance of new securities

Connected person refers to a person or a juristic person who has a relationship with the listed company in any of the following manners:

- The directors, executives, major shareholders, controlling person of the listed company, person to be nominated for directors, executive, or controlling person of the listed company, as well as their related persons and close relatives.

- Any juristic person with major shareholders or controlling persons in (1).

- Any person whose actions can be identified as proxy or under the influence of (1) and (2) regarding decision-making, policy-setting, management, or operations, or any other person with similar circumstances.

- The director of a juristic person with controlling power.

- The spouse, underage offspring or adopted child of the director in (4).

- A juristic person under the controlling power of the person in (4) or (5).

- Any person taking action under the perception or agreement that if the company enters into a transaction with such person, the following person will also gain similar benefit:

7.1 The company’s direct

7.2 The company’s executive

7.3 The company’s controlling person

7.4 The director of the person with controlling power over the compay

7.5 The spouse, underage offspring or adopted child of the person described in 7.1 to 7.4

Connected person refers to a person or a juristic person who has a relationship with the listed company in any of the following manners:

- The directors, executives, major shareholders, controlling person of the listed company, person to be nominated for directors, executive, or controlling person of the listed company, as well as their related persons and close relatives.

- Any juristic person with major shareholders or controlling persons in (1).

- Any person whose actions can be identified as proxy or under the influence of (1) and (2) regarding decision-making, policy-setting, management, or operations, or any other person with similar circumstances.

- The director of a juristic person with controlling power.

- The spouse, underage offspring or adopted child of the director in (4).

- A juristic person under the controlling power of the person in (4) or (5).

- Any person taking action under the perception or agreement that if the company enters into a transaction with such person, the following person will also gain similar benefit:

7.1 The company’s direct

7.2 The company’s executive

7.3 The company’s controlling person

7.4 The director of the person with controlling power over the compay

7.5 The spouse, underage offspring or adopted child of the person described in 7.1 to 7.4

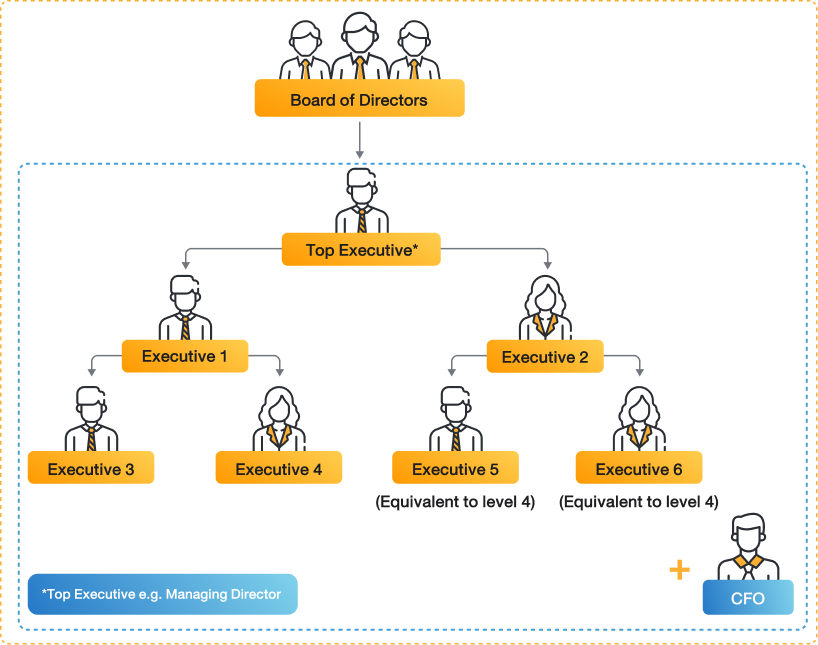

Executive refers to:

- The Manager (counting only the person holding the highest executive position)

- The first four executive officers ranking immediately below the Manager

- Every person holding a position equivalent to that of the fourth executive officer

- Executive officers in the accounting or finance department at the level of department manager or above, or equivalent (counting only the Chief Financial Officer - CFO).

Major shareholder refers to a direct and indirect shareholder of a juristic person with more than 10% holding of voting shares of the juristic person. This includes the holding of related person. In this regard, indirect shareholding means the holding of shares through other juristic persons in which such shareholder and their related persons consecutively hold shares down through all tiers, whereby the aggregate shareholding in each tier exceeds 30% of the total voting shares of such juristic person.

Related person means any individual or partnership who has a relationship with any person in any of the following manners, which includes:

- Spouse

- Underage children

- Ordinary Partnership where the person as well as (1) or (2) are partners

- Limited Partnership where the person as well as (1) or (2) are partners with unlimited liability or with limited liability provided that their holdings are over 30% of the total capital contribution of the limited partnership

- Limited company or public company where the person plus (1) or (2) or (3) or (4) collectively hold more than 30% of the total paid-up shares of that company

- Limited company or public company where the person plus (1) or (2) or (3) or (4) or (5) collectively hold more than 30% of the total paid-up shares of that company

- Juristic person in which such person has management power in the capacity of authorized representative of the juristic person

Controlling persons refer to the person with the controlling power over the company in any of the following manners, which means:

- Holding the voting shares of a juristic person more than 50% of the company’s total voting shares

- Having control over majority votes at the juristic person’s shareholder meeting, either directly or indirectly or by any reason

- Controlling an appointment or discharge of more than half of the directors, either directly or indirectly

Close relatives refer to the person having blood relations or legal relations by registration, who are:

- Father, Mother

- Siblings

- Children and spouse of the children

Transactions exempted from compliance with the related party transaction rules |

- Transactions under commercial agreements with general trading conditions approved by the Board of Directors, or in accordance with the principles approved by the Board of Directors.

General trading conditions means commercial terms that are fair and do not cause a transfer of benefits, in the same manner as a person of ordinary prudence would conduct with general counterparties under the same circumstances, with commercial bargaining power free from the influence of connected persons, as exemplified below:- - Prices and conditions applied to connected persons do not differ from those applied to other trading partners

(in cases where the company and the connected person regularly transact such goods/services with other trading partners). - - Gross profit margins and conditions applied to connected persons do not differ from those applied to other trading partners

(in cases of customized goods/services or job orders). - -In accordance with standard market prices

(in cases of goods/services with distinct and standardized market prices).

Procedure: In the case of entering into a related party transaction with general trading conditions, the company may seek approval for the commercial agreement or principles from the Board of Directors to enable the management to proceed, without requiring case-by-case approval for each related party transaction, provided that it complies with the general trading conditions or is not less favorable.

- - Prices and conditions applied to connected persons do not differ from those applied to other trading partners

- Granting of loans under the staff and employee welfare regulations.

- Transactions where the other counterparty of the listed company, or both counterparties, hold the status of a subsidiary in which the listed company holds not less than 90% of the total paid-up shares of such subsidiary.

- The listed company or its subsidiary issues new securities to related party in any of the following manners:

- 4.1 Related Parties receive securities through the exercise of rights in proportion to their shareholding (RO: Rights Offering), including offerings pursuant to a shareholders' meeting resolution to offer to all shareholders equally, excluding offerings that would impose duties under foreign laws on the company (PPO: Preferential Public Offering).

- 4.2 Related Parties act as underwriters on a firm commitment basis, provided that the criteria, terms, and conditions of such underwriting have been fully and clearly disclosed in the prospectus.

- 4.3 Received from the offering of securities under the Employee Stock Ownership Plan (ESOP) or executive stock option schemes.

- 4.4 Transactions entered into by the listed company or its subsidiary with a connected person who is a juristic person in which the listed company or its subsidiary is a shareholder, and has nominated a person to hold the highest executive position in such juristic person, provided that the listed company or its subsidiary and the said juristic person are not connected in any other manner.

Additional cases exempted from duties under the related party transaction rules |

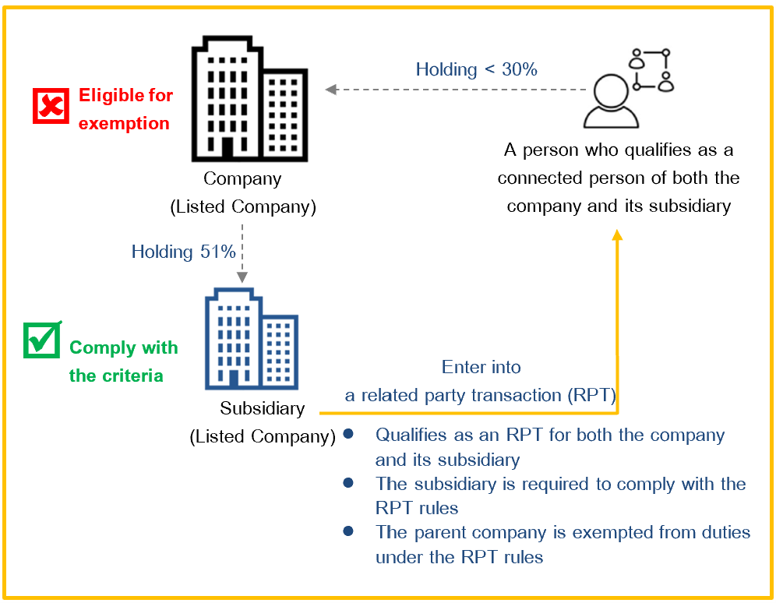

- Exemption from duties in the case where the subsidiary is a listed company

The listed company shall be exempted from duties under the related party transaction rules arising from transactions entered into by its subsidiary that is also a listed company (where such subsidiary shall be the sole party responsible for complying with the related party transaction rules arising from the said transaction).

In considering the entering into of the said related party transactions, the Board of Directors of both the listed company and its subsidiary must perform their duties with responsibility, due care, and loyalty in accordance with fiduciary duties, primarily taking into account the best interests of their respective companies.

To ensure transparency and prevent conflicts of interest, the listed company and its subsidiary may consider implementing either of the following guidelines:

Guideline 1: The listed company shall not participate in the consideration and approval of the subsidiary’s transactions.

To ensure transparency and prevent conflicts of interest, the listed company and its subsidiary may consider implementing either of the following guidelines:

Guideline 1: The listed company shall not participate in the consideration and approval of the subsidiary’s transactions.

- - The listed company’s representatives on the Board of Directors of the subsidiary shall not attend the subsidiary’s Board of Directors’ meeting, which is held to consider and approve the transaction, and shall have no voting rights at the meeting.

- - The shares held by the listed company shall not be counted as voting shares for the agenda item concerning the consideration and approval of the transaction at the subsidiary’s shareholders’ meeting.

- - Interested directors (such as connected persons involved in the transaction, close relatives and related persons of the said connected persons, or persons nominated as representatives on the Board of Directors by the said connected persons) shall not attend and shall have no voting rights at the listed company’s Board of Directors’ meeting held to determine the voting direction for approving the transaction at the Board of Directors’ or shareholders’ meetings of the subsidiary.

- - The exercise of voting rights by the listed company at the Board of Directors’ or shareholders’ meetings of the subsidiary shall strictly follow the resolution passed by the listed company’s Board of Directors, which must be free from any influence of the connected persons involved in the transaction.

Consideration and Compliance with related party Transaction Rules |

- Determine whether the transaction qualifies as a related party transaction that is subject to the related party transaction rules.

- Calculate the transaction size based on the prescribed criteria as of the date on which the Board of Directors passed the resolution regarding the matter.

- Seek approval for the transaction and execute the duties prescribed by the rules according to the calculated transaction size. In this regard, the transaction size shall include any other transactions entered into with the same connected person or group within a prior 6-month period, which shall be accumulated into the same transaction, except for transactions that have already received approval from the shareholders' meeting.

If the said related party transaction also qualifies as a material transaction (Asset Acquisition or Disposal), compliance with the material transaction criteria is also strictly required.

Calculation of the transaction size and accumulate the transaction value |

- Calculation of Related Party Transaction Size

Normal Cases

The company should measure the size of related party transaction to determine the subsequent actions required under the rules. The company should compare the transaction value against the higher one between the two references as per the latest financial statement (X is the transaction value):

| Transaction size | Authorized approver | Choose the maximum value between | |

| Small | No regulatory requirement | X ≤ 1 million Baht | X ≤ 0.03% NA* |

| Medium | Board of Directors | 1 million Baht < X < 20 million Baht | 0.03%NA* < X < 3% NA* |

| Large | Shareholders' meeting | X ≥ 20 million Baht | X ≥ 3% NA* |

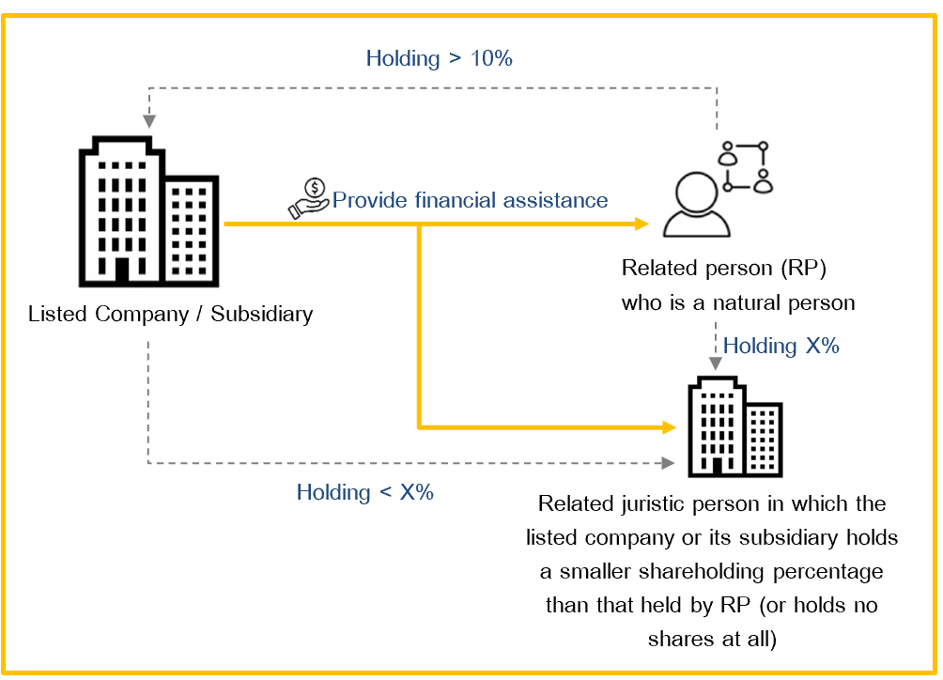

- Special Cases

Specifically, the provision of financial assistance to the following connected persons:- A natural person

- A juristic person in which the listed company or its subsidiary holds a smaller shareholding percentage than other connected persons;

- A juristic person in which the listed company or its subsidiary holds no shares

The Company shall calculate the transaction size to determine the actions required under the rules by comparing the transaction value against the lower of the two reference amounts based on the latest financial statements (where "X" represents the transaction value) as follows:

| Authorized approver | Choose the minimum value between | |

| Board of Directors | X < 100 million Baht | X < 3% NA* |

| Shareholders' meeting | X ≥ 100 million Baht | X ≥ 3% NA* |

* Net Asset Value (NA) (Attributable to the parent company) means

Total Assets – Total Liabilities – Non-controlling interests (if any).

In the case where the company prepares consolidated financial statements, NA according to the latest consolidated financial statements that have been audited or reviewed by the auditor shall be used.

Total Assets – Total Liabilities – Non-controlling interests (if any).

In the case where the company prepares consolidated financial statements, NA according to the latest consolidated financial statements that have been audited or reviewed by the auditor shall be used.

- Guidelines for the Calculation of Transaction Value

| Transaction Type | Value Used for Transaction Size Calculation | Example |

| 1. Provision of Financial Assistance | - The principal and interest calculated throughout the entire loan period, or the total value of the guarantee, or the potential damages that may occur to the listed company or its subsidiary if the connected person defaults on the debt. - The interest value shall be calculated based on the interest rate charged to the connected person or the average borrowing interest rate of the company or its subsidiary, whichever is higher. | A loan of 20 million Baht for a 2-year term at an interest rate of 5%. The value used for the transaction size calculation is 22 million Baht (20+(20x5%x2)) |

| 2. Receipt of Financial Assistance | The value of interest and benefits that the listed company or its subsidiary must pay to the connected person throughout the period of receiving such financial assistance. | A loan of 20 million Baht for a 2-year term at an interest rate of 5%. The value used for the transaction size calculation is 2 million Baht (20x5%x2) |

| 3. Disposal of Investment Resulting in Termination of Subsidiary Status | The total value of consideration to be received, including any outstanding loans (both principal and interest), financial guarantees, or other outstanding obligations due to the listed company or its subsidiary. | The disposal of all investments in a subsidiary to a major shareholder for 100 million Baht, where the subsidiary has an outstanding loan plus accrued interest due to the listed company of 50 million Baht. The value used for the calculation is 150 million Baht. |

| 4. Other Transactions | The total value of consideration paid or received, or the book value, or the market value (fair value), whichever is higher. | The sale of land with an agreed selling price of 200 million Baht, where the land has a book value of 150 million Baht and an appraised value by an independent appraiser of 198 million Baht. Therefore, the value used for the calculation is 200 million Baht. |

Note: If the said related party transaction also qualifies as a Material Transaction (MT), the related party transaction size must be calculated in alignment with the additional guidelines for transaction value calculation under the "Total value of consideration paid or received”.

- Accumulation of Transaction Value

Transactions entered into with the same connected person or group within a prior 6-month period : must be accumulated (excluding related party transactions that have already been approved by the shareholders' meeting).

Same Connected Person or Group: Refers to connected persons of the listed company who are related in the following manners:

(1) The same connected person;

(2) Major shareholders, controlling persons, related persons, and close relatives of the person under (1);

(3) Related persons and close relatives of the person under (2);

(4) A juristic person whose major shareholder or controlling person is the person under (1), (2), or (3).

Note: The SEC has the authority to accumulate various transactions into a single transaction if the facts indicate that the company intended to split the transactions into multiple items to circumvent compliance with the prescribed rules.

Required Actions Based on Transaction Size |

- Execute required actions in accordance with the calculated transaction size

| Related Party Transaction | Authority | ||

| Small | Medium | Large | |

| 1. Normal cases | No regulatory requirement. (Subject to the Company’s internal delegation of authority) | Board of Directors + Disclose information via the SETLink system. | Board of Directors + Disclose information via SETLink + Seek shareholders' approval* (With an IFA opinion provided to the shareholders) + Submit progress reports on the transaction. |

2. Special Case | Board of Directors + Disclose information via the SETLink system. | - | Board of Directors + Disclose information via SETLink + Seek shareholders' approval* (With an IFA opinion provided to the shareholders) + Submit progress reports on the transaction |

* In the case of seeking shareholders' approval:

- - Appointment of an Independent Financial Advisor (IFA)

An IFA must be appointed to provide an opinion on the entering into of such transaction. The IFA must express opinions on various matters, such as the reasonableness and benefits of the transaction to the Company, the fairness of the price and transaction conditions, and the associated risks. - - Shareholders' Resolution Requirements

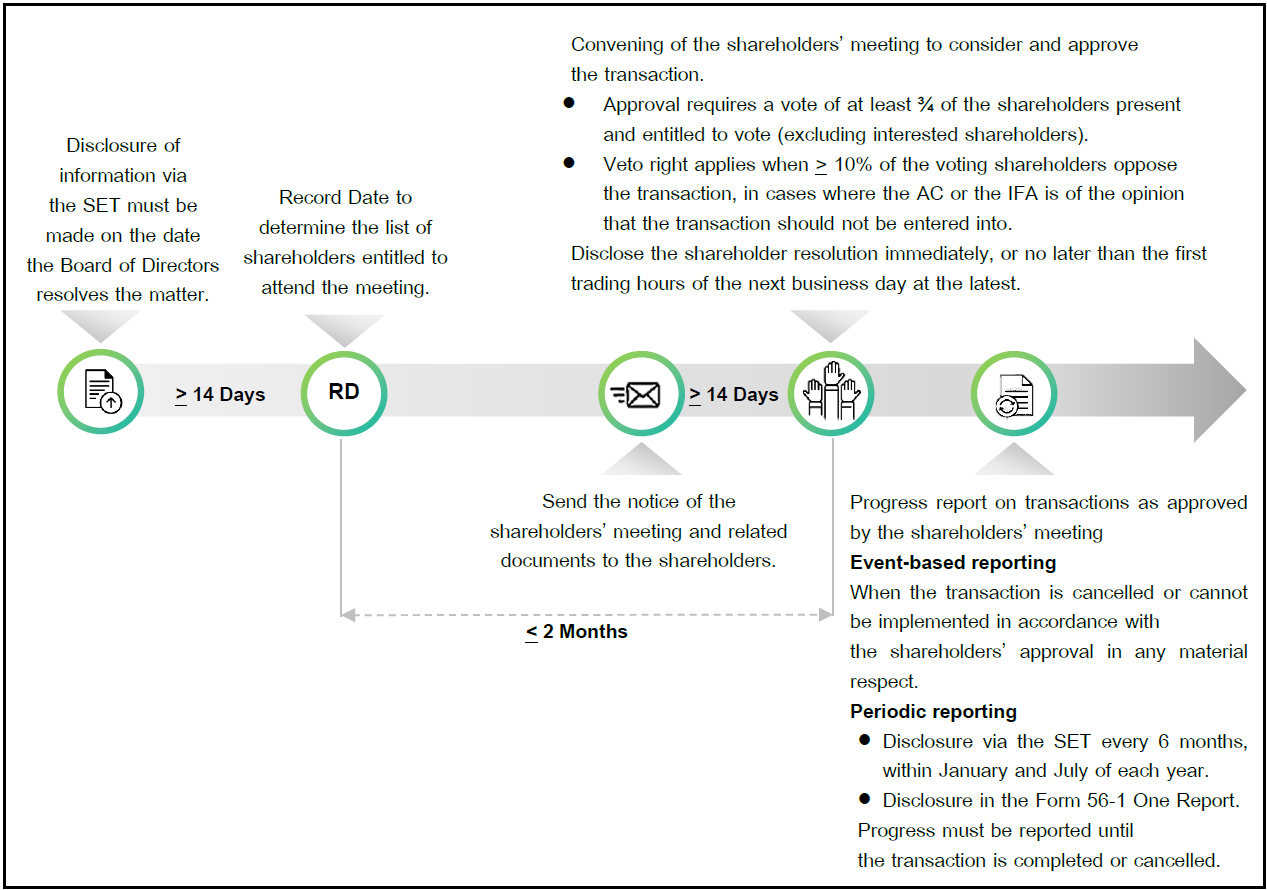

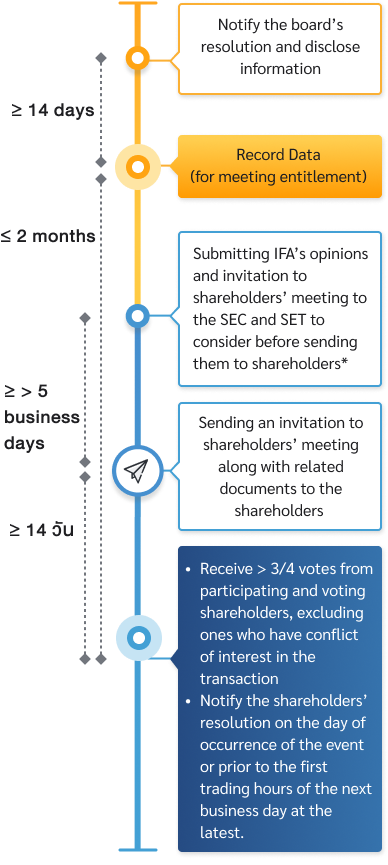

Approval from the shareholders' meeting requires a majority vote of not less than three-fourths (3/4) of the total votes of the shareholders who are present at the meeting and entitled to vote, excluding the votes of interested shareholders. - - Right to Object and Veto the Transaction

In the event that the IFA or the Audit Committee opines that the transaction should not be entered into, shareholders collectively holding more than 10% of the total votes of the shareholders present and entitled to vote can cast an objecting vote to veto the transaction.

Information disclosure |

- The company has to notify, via SETLink, about the board resolutions on the related party transactions immediately upon making the transaction (normally on the day the board has given an approval), that is within the day the board has made the resolution or prior to the first trading hours of the next business day at the latest.

- Key information of the board resolution are:

- (A) The nature and details of the transaction must be disclosed, including at least the following matters:

- 1) Date, month, year or the expected timeline for the transaction

2) Name of the counterparty (contracting party) involved and relationship with the listed company or its subsidiaries, including a specification of the relationship that qualifies the aforementioned person as a connected person of the Company.

3) General characteristics of the transaction, including detailed information such as the transaction overview, execution, objectives, as well as the relevant procedures, terms, and conditions.

4) Details of the assets involved in the transaction, including the characteristics and operational condition, as well as any encumbrances on the assets. In the case of securities, please provide general corporate information, such as business nature, registered capital, paid-up capital, a summary of financial position and operating results for the past 3 years, a list of the board of directors, and a list of the top 10 shareholders along with their shareholding percentages, including the ultimate shareholders of the said entity. Furthermore, if any connected persons of the company hold shares in the said entity, please specify their names along with their shareholding percentages.

5) Total value of the transaction and details of payment terms, including specification of relevant terms and agreements, such as the timeframe or installment plan for payment, and deposit placements. In the event that the consideration paid for the transaction is non-cash (e.g., issuance of securities to pay for asset acquisition or asset swap), please specify the type and details of the securities or assets used as consideration, along with the method used to determine the value of such consideration.

6) Transaction Size Calculation: Please specify: 1. The calculation method for the transaction size in accordance with the related party transaction criteria, and 2. The maximum calculated transaction size, including the company’s obligations and duties of disclosure in compliance with the relevant regulations.

7) The source of fund for entering transaction or the plan for utilizing the proceeds received from the transaction. In the event that financing is obtained from a financial institution for the transaction, please specify the possible conditions that may affect the shareholder rights must be specified such as the limitation to pay dividend.

8) In the event that the company invests in a business where a connected person of the listed company holds more than 10% of the total voting rights, and such business becomes an associate or a subsidiary after the transaction, the company must explain the rationale behind this shareholding structure, demonstrate how it serves the best interests of the company, and specify preventive measures against potential conflicts of interest that may arise in the future.

9) The company shall disclose the opinions of independent experts, such as asset appraisers and financial advisors, if any such opinions are applicable to the transaction.

10) A summary of the key terms and conditions of all relevant material agreements must be provided.

11) In cases where a transaction requires approval from relevant regulatory authorities, related details must be disclosed, including the name of regulatory authorities, applicable laws and regulations, conditions for approval, as well as the timeline for the application process.

12) The company must disclose any outstanding legal disputes related to the transaction or the assets to be acquired or disposed of, if applicable.

13) Any other information that may significantly affect investors' decision-making processes must be fully disclosed

- (B) The business plan related to the transaction must be disclosed, including the following items:

- 1) Policies and business plans related to the transaction, including a brief timeline.

2) Analysis of market conditions, competition, and business opportunities.

3) Risk factors or events potentially preventing execution according to the plan.

4) Contingency plan for an unsuccessful transaction and analysis of potential impacts.

- (C) Opinions of the Board of Directors on at least the following matters:

- 1) Reasonableness and benefits of the transaction

2) Potential risks or impacts from the transaction

3) Appropriateness of the price and conditions

For related party transactions, an analysis of the reasonableness and benefits compared to a transaction with a third party is required.

- (D) The Board of Directors must provide a certification stating that they have reviewed and examined the relevant information with due care, and are of the opinion that the transaction is reasonable and in the best interests of the company and its shareholders.

- (E) The Audit Committee shall provide its opinion regarding the transaction, explicitly explaining whether it aligns with or differs from the opinion of the Board of Directors, along with the supporting rationale.

(F) The company must certify that directors with a vested interest in the related party transaction did not attend the meeting and did not vote during the Board of Directors' approval process. (In case of necessity, interested directors may enter to provide explanations or information, but must not be present during deliberation and voting on that agenda item).

- (E) The Audit Committee shall provide its opinion regarding the transaction, explicitly explaining whether it aligns with or differs from the opinion of the Board of Directors, along with the supporting rationale.

Comments of independent financial advisor (IFA) |

For transactions that require an Independent Financial Advisor (IFA) opinion report to support the shareholders' meeting consideration under the related party transaction rules, such IFA report must contain at least the following items:

- A brief summary and overview of the transaction, with references permitted to the detailed information disclosed by the company in the notice of the shareholders' meeting.

- The IFA’s opinions addressing at least the following matters:

A) Reasonableness and benefits of entering into the transaction.

B) Potential risks or impacts that may arise from the transaction.

C) Appropriateness of the transaction price and conditions.

In providing these opinions, the IFA must present supporting data along with explanations of the underlying rationale and key assumptions. Additionally, a comparative analysis of the pros and cons between entering into the transaction with a connected person versus an independent third party must be included.

- A conclusion of the IFA’s opinion on whether the shareholders should approve or disapprove the transaction, together with supporting reasons.

- A certification of duty performance stating that the IFA has performed its duties with due care and diligence in accordance with professional standards, putting the best interests of the company's shareholders as the primary consideration.

Sending a notice of the shareholders' meeting to the shareholders |

The company must dispatch the notice of the shareholders' meeting to shareholders at least 14 days prior to the meeting date, and simultaneously disclose the notice via the SETLink system, with at least the following minimum requirements:

- The minimum requirements are disclosed in the information memorandum regarding the transaction (disclosed via the SETLink system).

- The names and the number of shares held by interested shareholders who are not entitled to vote.

- Proxy forms that allow shareholders to cast their votes, along with nominating at least one member of the audit committee to act as a proxy for the shareholders.

- In the event that the audit committee or the IFA is of the opinion that shareholders should not approve the transaction, the details regarding the shareholders' rights to object to the transaction must be specified.

- The Independent Financial Advisor (IFA) opinion report.

Progress reporting (Shareholder-approved transactions only) |

A listed company is required to report the progress of the transaction through SETLink, as prescribed by the SEC, only for transactions that have been approved by the shareholders.

- Event-based reporting : The company must report immediately within the next business day from the date on which it knew or should have known of such event when:

- the transaction is cancelled; or

- the company is unable to proceed with the transaction as approved by the shareholders in any material respect, such as changes to the transaction timeline, transaction conditions, counterparties, transaction value, etc. - Reporting must continue until the transaction is completed or cancelled.

Reporting schedule and disclosure channels

| Reporting period | Reporting timeline | Disclosure channel |

| 6-month reporting period | By 31 January and 31 July of each year | Disclose information via the SETLink system |

| 1-year reporting period | Within 3 months from the end of each fiscal year-end period | Form 56-1 One report |

Information to be Disclosed

| Transaction | Type of Transaction | Date of approval | Summary of the transaction | Progress status | |

| Transaction sequence | Specify transactions that are: Note: For transactions that have been completed or cancelled during the current reporting period, the company is not required to continue reporting their progress in subsequent reporting periods. | Specify whether the transaction is a material transaction, a related party transaction, or falls under both categories. | Specify the date of approval from the shareholders’ meeting. | Provide a brief summary of the transaction as approved by the shareholders’ meeting. | - Specify the latest progress status as of the present date. |

Process of getting approval on connected transactions from the shareholders’ meeting

Related Regulations

|

|

|

|

Connected Transactions