Share Repurchase

One of the financial instruments to manage a company's liquidity when its share price is below the fair value and its retained earnings and financial liquidity exceed what is needed to run the business at the time. The treasury shares will not be counted as a quorum in the shareholders' meeting and will not be entitled to vote or dividends.

Benefits of Share Repurchase

Company

| Increase stock demand, which may lead to a share price increase |

| Reduce the number of shares on the market, resulting in higher earnings per share |

| Can use it as an effective tool to manage excess liquidity |

| Capitalize on a capital gain if the company is confident in its future performance and believes that its share price is significantly lower than its fundamental value, reselling shares at the right time will generate profitable returns, with the capital gain recorded in the shareholders' equity as a premium on treasury shares |

Shareholders

| Earnings per share (EPS) and Return on Equity (ROE) are higher because repurchased shares are not factored into the EPS calculation |

| Have opportunities of receiving a higher dividend per share |

| There is also a possibility that the share price will rise due to the higher earnings per share |

Public Limited Companies Act contains provisions which allow a company to own its own shares in 2 cases, namely:

| In case the shareholders vote against the resolution of shareholders’ meeting to amend the company’s articles of association in the matters related to voting rights or rights to receive dividends; and | ||

| For the purpose of financial management when the company has accumulated profit and excess liquidity. | ||

- Share repurchase is permitted under the articles of association of the company:

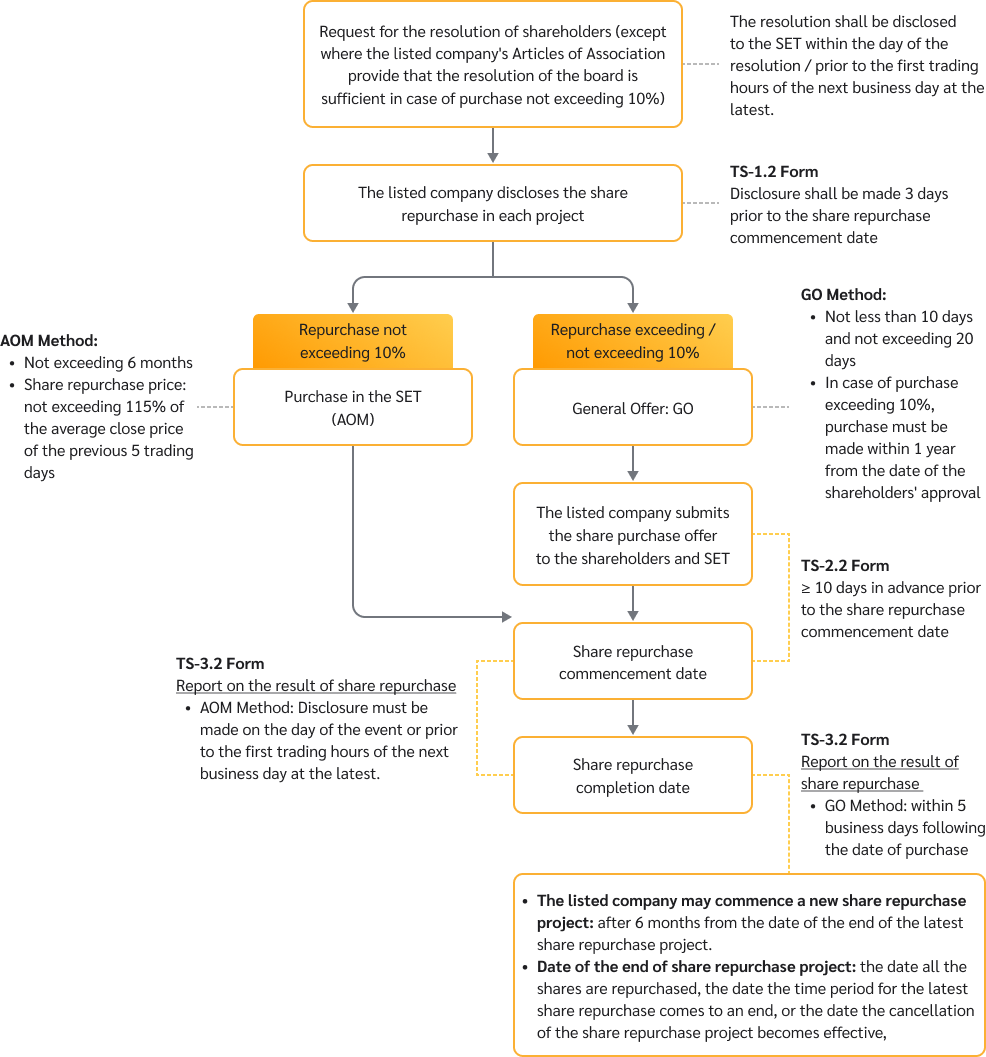

- If the repurchase of shares ≤ 10% of the paid-up capital, the board of directors may be granted the power to determine the repurchase of shares.

- If the repurchase of shares >10% of the paid-up capital, approval from the shareholders’ meeting must be obtained and the shares must be repurchased within 1 year.

Additionally, a listed company who will repurchase shares for the purpose of financial management shall also have the following qualifications:

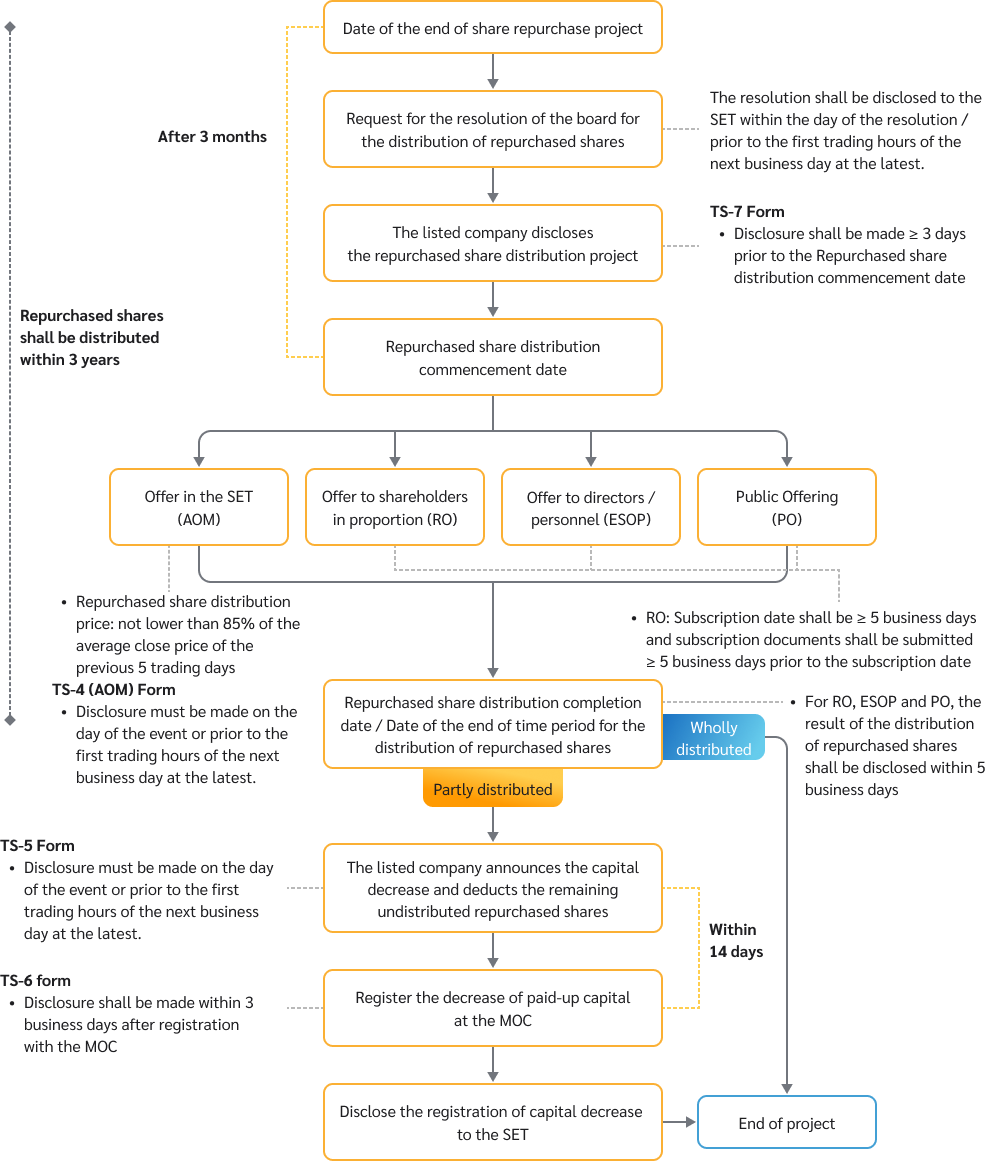

- Have accumulated profit on the separate financial statement: the repurchase limit shall not exceed the company’s unappropriated accumulated profit which shall be reserved until the repurchased shares are wholly distributed or upon the decrease of capital to deduct the remaining repurchased shares after the distribution;

- Have excess liquidity: considering from the ability to repay the debts within the next 6 months from the date of the share repurchase commencement date and the share repurchase does not affect the company’s ability to repay debts; and

- Free float proportion must not be reduced to lower than the minimum threshold stipulated by SET i.e. namely, not lower than 15% of the paid-up capital, and not less than 150 minority shareholders.

The method for share repurchase in each case is as follows:

| 1 | In case of share repurchase in case the shareholders vote against the resolution of shareholders’ meeting to amend the company’s articles of association in the matters related to voting rights or rights to receive dividends: the company shall adopt General Offer method (General Offer : GO). | ||||||||||

| 2 | There are 2 methods in case of share repurchase for the purpose of financial management:

| ||||||||||

|

- Repurchase price ≤ 115% of the average close price of the previous 5 trading days

- Distribution price ≥ 85% of the average close price of the previous 5 trading days

| 1. | Upon the passing of board of directors’ resolution on the share repurchase on Day T |

| In case the shareholders vote against the resolution | In case of financial management |

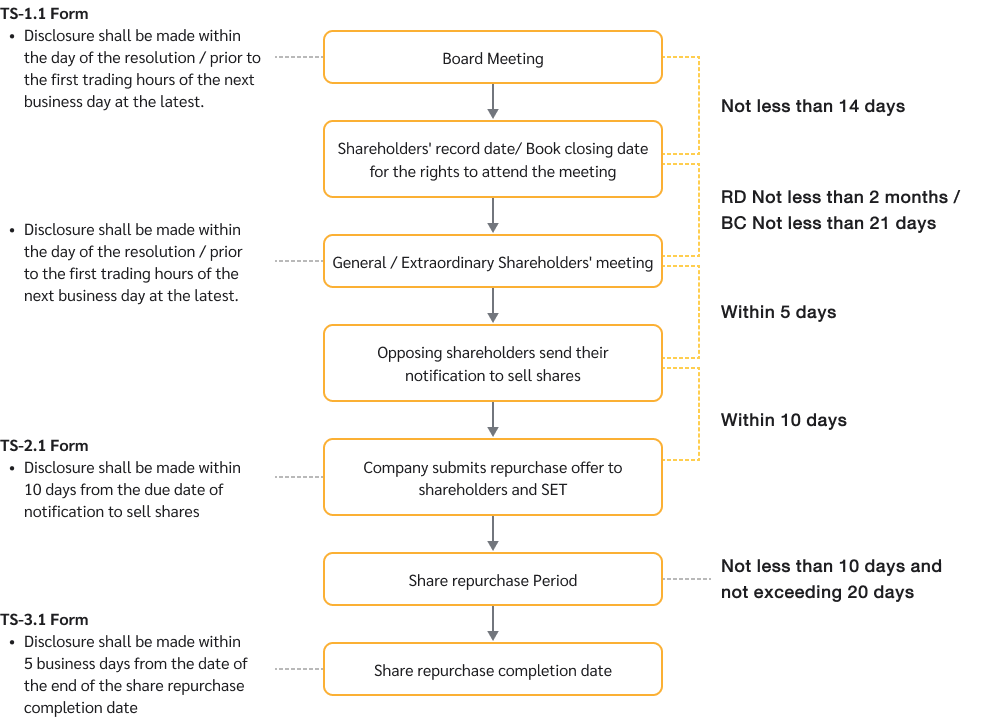

1. Period where the resolution must be disclosed

| 1. Period where the resolution must be disclosed

|

2. Information that must be disclosed (Form TS-1.1)

| 2. Information that must be disclosed (Form TS-1.2)

|

- Listed company shall disclose the share repurchase project or distribution of repurchased shares 3 days before the commencement date of share repurchase / distribution of repurchased shares / the date the amendment or cancellation of the share repurchase project comes into effect. The disclosure must be done without delay on the date of the board of directors’ or shareholders’ resolution, as the case may be, and in case of amending or cancelling the project, the reason and necessity for such amendment or cancellation shall also be disclosed (Form TS-3).

- For offer for share repurchase in case the shareholders vote against the resolution to amend the company’s articles of association in the matters related to voting rights / rights to receive dividends and the general offer for share repurchase for the purpose of financial management, the offer for share repurchase form shall be submitted to the shareholders and submitted via SETLink system to be disclosed to investors as follows:

- In case the shareholders vote against the resolution, offer for share repurchase form (Form TS-2.1) shall be submitted to the shareholders who vote against the resolution within 10 days from the date the period for notifying the offer has expired whereby the repurchase time period shall be 10 - 20 days.

- In case of general offer for share repurchase for the purpose of financial management, the offer for share repurchase form (Form TS-2.2) shall be submitted to the shareholders 10 days before the share repurchase commencement date whereby the repurchase time period shall not be less than 10 - 20 days.

| 2. | Report on the result of share repurchase |

| In case the shareholders vote against the resolution and in case of general offer | In case of share repurchase via SET |

1. Period of disclosure

| 1. Period of disclosure

|

2. Information that must be disclosed (Form TS-4 : Template available on the SETLink system)

| 2. Information that must be disclosed (Form TS-4 : Template available on the SETLink system)

|

| 3. | Upon the passing of board of directors’ resolution on the distribution of repurchased shares on Day T |

| In every case |

1. Period of disclosure

|

2. Information that must be disclosed (Form TS-7.1)

|

- In case distribution of repurchased shares via RO: To proceed the same as in the case of Right Offering for newly issued shares i.e. the listed company shall disclose the date for share subscription to the existing shareholders not less than 14 days in advance including sending notice of rights >5 business days in advance and stipulate period for subscription > 5 business days etc.

- In the event of any amendment, cancellation, or extension of the period for the resale of repurchased shares, the company shall disclose such information without delay on the date the resolution is passed by the Board of Directors or the shareholders, as the case may be, together with the reasons and necessity for such action (Form TS-7.2).

| 4. | Report on the result of distribution of repurchased shares |

| In case of offer via PO, RO or ESOP | In case of distribution via SET |

1. Period of disclosure

| 1. Period of disclosure

|

2. Information that must be disclosed

| 2. Information that must be disclosed (Form TS-4 : Template available on the SETLink system)

|

| 5. | Upon the passing of board of directors’ resolution on the deduction of the repurchased shares and capital decrease on day T |

| In every case |

1. Period of disclosure

|

2. Information that must be disclosed (Form TS-5)

|

| 6. | Upon the completion of capital decrease registration with the Ministry of Commerce by the company |

| In every case |

1. Information that must be disclosed (Form TS-6) within 3 business days after the capital decrease registration

|

The company can commence the new share repurchase program upon the completion of the full amount of the share repurchase, or upon the expiration of the period specified for the previous share repurchase program, or from the effective date of the cancellation of the previous share repurchase program.

1. Procedures for Share Repurchase In case the Shareholders vote against the Resolution of the Shareholders' Meeting

2. Procedures for Share Repurchase for Financial Management

1 The total number of shares that the company repurchases and holds at any time shall not exceed 20% of the total issued shares of the company. In the case where the total number of repurchased shares held by the company exceeds the specified amount, the company must dispose of the portion of repurchased shares exceeding 20% within 3 months. Otherwise, the company shall reduce its paid-up capital by canceling the excess repurchased shares.

| Note : | - In case of the amendment to or cancellation of the share repurchase, the listed company shall disclose the information ≥ 3 days in advance prior to the date the amendment becomes effective (Form TS-3). - AOM (Automatic Order Matching) is a purchase method by means of automatic matching via the trading system of SET |

3. Procedures for the Distribution of Repurchased Shares

2 In the case where the company is unable to dispose of the repurchased shares within 3 years from the completion of the share repurchase, and the weighted average market price of the company’s shares during the 3-month period prior to the date on which the Board of Directors resolves to convene a shareholders’ meeting is lower than the average repurchase price, the company may extend the period for the disposal of the repurchased shares for an additional period not exceeding 2 years. Such extension of the disposal period shall be subject to the approval of the shareholders’ meeting obtained prior to the expiry of the original disposal period specified in the share repurchase program.

| Note : | - In case of amendment to the repurchased share distribution method, the listed company shall disclose the information ≥ 3 days in advance prior to the date the amendment becomes effective (Form TS-7.2). - The offer for sale by via ESOP and PO methods shall be in accordance with the rules of the Office of the SEC. |

Related regulations

|

|

|

|

|

Forms

| Report on Disclosure of Share Repurchase Information comprising the following : |

|

|

|

|

|

|

|

|

|

|

FAQ

|