The Securities and Exchange Act B.E. 2535, amended version, effective on August 31, 2008 (Section 89/29), prescribed the Securities and Exchange Commission (SEC) to specify details and monitor the transactions on assets acquisition and disposition of the listed companies. The SEC has thus issued the Capital Market Supervisory Board Announcement Tor.Jor. 20/2551 about the regulation on significant transactions subjecting to be an acquisition or disposition of assets that the listed companies should be abide by as per SET’s requirement.

Currently, the SEC has revised the existing regulations to provide greater clarity, align them with current circumstances, and further enhance investor protection. Accordingly, the Capital Market Supervisory Board has issued Notification No. TorJor. 45/2568 Re: Rules on Material Transactions, which is effective on 1 July 2026 onwards.

Material Transactions refer to transactions entered into by a listed company* or its subsidiary that fall within the prescribed categories and involve a transaction size or value at a level that may materially affect the company’s financial position, operating results, or shareholders’ rights. Therefore, in order to protect shareholders’ interests, the relevant regulations require listed companies to disclose information to shareholders and provide shareholders with an opportunity to participate in the consideration and decision-making process regarding such transactions.

* Applicable only to companies listed on the SET/mai (excluding LiVEx), and also includes companies whose common shares have been delisted but which still have obligations to prepare and submit reports on financial position and operating results under Section 56 of the Securities and Exchange Act.

Currently, the SEC has revised the existing regulations to provide greater clarity, align them with current circumstances, and further enhance investor protection. Accordingly, the Capital Market Supervisory Board has issued Notification No. TorJor. 45/2568 Re: Rules on Material Transactions, which is effective on 1 July 2026 onwards.

Material Transactions refer to transactions entered into by a listed company* or its subsidiary that fall within the prescribed categories and involve a transaction size or value at a level that may materially affect the company’s financial position, operating results, or shareholders’ rights. Therefore, in order to protect shareholders’ interests, the relevant regulations require listed companies to disclose information to shareholders and provide shareholders with an opportunity to participate in the consideration and decision-making process regarding such transactions.

* Applicable only to companies listed on the SET/mai (excluding LiVEx), and also includes companies whose common shares have been delisted but which still have obligations to prepare and submit reports on financial position and operating results under Section 56 of the Securities and Exchange Act.

Definition |

Subsidiary means a limited company or a public limited company that is under the control of a listed company in any of the following manners (including all successive tiers throughout the chain) as follows:

- Holding voting shares exceeding 50% of the total voting rights

- having the power to control the majority of votes at the shareholders’ meeting of a juristic person, whether directly or indirectly, or by any other means

- having the power to control the appointment or removal of at least half of the total directors, whether directly or indirectly.

Note: The definitions of “subsidiary” and “control” are referenced from Section 89/1 of the Securities and Exchange Act. A company classified as a subsidiary under such definitions may differ from the criteria under accounting standards.

Transactions Subject to the Rules on Material Transactions

Entering into, or agreeing to enter into, any contract, arrangement, or understanding, whether directly or indirectly, that results in any of the following transactions:

- the acquisition or disposal of assets or

- the transfer or waiver of benefits, including the waiver of claims against a person causing damage to the listed company, whether such benefits are related to the assets of the listed company or its subsidiary.

- the execution, amendment, or termination of agreements relating to the lease or hire-purchase of all or part of a business or assets.

- the granting of loans, provision of credit facilities, guarantees, execution of juristic acts causing the company to incur additional financial obligations in cases where an external party lacks liquidity or is unable to repay debts, or the provision of any other forms of financial assistance to another person.

Exempted Transactions |

- Acquisition or disposal of current assets used in the ordinary course of business, such as raw materials, inventories, and consumable supplies.

- Liquidity management, including:

- investments in low-risk financial assets, such as government bonds, debt instruments fully guaranteed by the Ministry of Finance, and units in money market funds or fixed income funds; provided that investments in other financial assets must not result in the company being classified as an investment company.

- share repurchases - Transactions between a listed company and its subsidiary, or between subsidiaries.

- Establishment of a subsidiary.

- The following transactions conducted in the ordinary course of business of the listed company or its subsidiary are exempted:

- The following transactions conducted in the ordinary course of business of the listed company or its subsidiary are exempted:

- Granting loans, extending credit, providing guarantees, entering into juristic acts that result in the company assuming additional financial obligations in cases where external parties lack liquidity or are unable to perform debt repayment obligations, or providing any other forms of financial assistance to other persons, where such activities are conducted in the ordinary course of business of the company or its subsidiary.

Consideration of Material Transactions |

1. Consider whether the transaction falls within the scope requiring compliance with the rules on material transactions.

2. Calculate the size of transaction as of the day when the board of directors has reached a resolution

3. The highest transaction size shall be applied for compliance purposes, taking into account the aggregate size of related transactions or transactions undertaken under the same project during the 12-month period preceding the date of entry into the transaction, excluding transactions that have already been approved by shareholders.

Therefore, if the counterparty is connected person, the procedure should be in line with the connected transactions rule.

Calculation of the transaction size |

- Calculate the size of transaction to evaluate its potential effects on the company’s financial positions and operational performance in various aspects

- Four bases of calculation:

| Type of assets | Acquisition or disposal of shares in a juristic person | Other cases | ||

| Method of payment | Cash | Share issue | Cash | Share issue |

| Basis of transaction size calculation | ||||

| 1. Value of the net assets | | | ||

| 2. Net profits | | | ||

| 3. Total value of consideration paid or received | | | | |

| 4. Value of securities issued | | | ||

How to calculate a transaction size for each basis |

Normal case

1. Calculation based on the value of net assets

- Calculation formula :

1. Calculation based on the value of net assets

- Calculation formula :

(NA* of investee company x Proportion of assets acquired or disposed) x 100

NA* of the listed company

* Net assets (NA) = total assets – total liabilities – non-controlling interests (if any)

Note:

- In case the company produces consolidated financial statements, use NA from consolidated financial statements.

- The latest financial statements (audited or reviewed) shall be used for calculation purposes. The latest financial statements of the listed company and the investee company may be for different reporting periods.

- If the NA of the listed company is negative, the transaction value based on the NA criterion shall not be calculated.

Note:

- In case the company produces consolidated financial statements, use NA from consolidated financial statements.

- The latest financial statements (audited or reviewed) shall be used for calculation purposes. The latest financial statements of the listed company and the investee company may be for different reporting periods.

- If the NA of the listed company is negative, the transaction value based on the NA criterion shall not be calculated.

2. Calculation based on net profits

- Calculation formula:

- Calculation formula:

(Net profits for the latest 4-quarters of the investee company x Proportion of assets acquired or disposed) x 100

Net profits for the latest 4-quarters of the listed company

Note:

- In case the company produces consolidated financial statements, use NA from consolidated financial statements.

- The latest financial statements (audited or reviewed) shall be used for calculation purposes.

- The latest financial statements of the listed company and the investee company may be for different reporting periods.

- If the listed company records a net loss, the transaction value under the net profit criterion shall not be calculated.

3. Calculation based on total value of consideration paid or received

- Calculation formula:

- Calculation formula:

Value of transaction paid or received* x 100

Total assets of listed company

*1) In the case of disposal of securities or issuance of securities as consideration, the highest value among the following shall be used:

1.1) Value of the consideration.

1.2) Book value (Net asset value) according to the issuer's latest financial statements (audited or reviewed).

- In the case where a listed company or its subsidiary disposes of securities held in another company, the financial statements of such company shall be used.

- In the case where a listed company or its subsidiary issues securities as consideration for the acquisition of assets, the financial statements of the issuing listed company or subsidiary shall be used.

1.3) Market value (in case of listed securities), utilizing the volume-weighted average price for 7-15 consecutive business days prior to the date of the Board of Directors' resolution approving the transaction.

1.4) Fair value prepared by a financial advisor (FA), if such valuation has already been prepared for decision-making purposes.

2) In the case of disposal of other assets (non-securities), value of the shares sold shall be based on the highest value among the following shall be used:

2.1) Value of the consideration (agreed transaction price).

2.2) Book value of the disposed assets based on the latest financial statements of the listed company (audited or reviewed).

2.3) Appraised value of the assets conducted by an appraiser approved by the SEC (the appraisal should not be older than 12 months).

3) In the case of disposal of shares in a subsidiary, or waiver of rights resulting in the loss of subsidiary status, value of the shares sold shall be based on the highest value among the following shall be used:

3.1) Selling price.

3.2) Book value of the shares corresponding to the disposed portion.

In addition, all financial assistance provided and all outstanding obligations of such company owed to the listed company shall be included in the calculation.

4) Entering into, amendment, or termination of any agreement relating to the lease or hire-purchase of a business or non-core asset of the listed company or its subsidiaries; the transaction value shall be calculated in accordance with the following methods:

4.1) Lease: calculated based on the total lease payments over the contract term, or the expected lease period (not required to calculate NPV).

4.2) Hire-purchase: calculated based on the total principal and interest over the contract term.

Note:

*Lease (lessee side): calculated based on the total lease payments over the contract term, or expected lease period (not required to calculate NPV).

*Hire-purchase (lessee side): calculated based on the purchase price of the asset, excluding interest.

However, in case of considering the renewal of a lease or rental agreement, the purpose, intent of the transaction, and the nature of the investment must be taken into account.

5) The provision of loans, credit facilities, guarantees, or entering into legal acts that bind the company to additional financial burdens for other persons, which are not in the ordinary course of business of the listed company or its subsidiaries.

The transaction value shall be calculated based on the principal amount plus total interest over the contract term, or the guarantee amount, or the potential loss in case of non-repayment, whichever is applicable.

Interest shall be calculated using either the contractual interest rate or the average borrowing rate of the listed company or its subsidiary, whichever is higher.

4. Calculation based on value of equity shares issued

- Calculation formula:

- Calculation formula:

Equity shares issued for the payment of assets x 100

Issued and paid-up shares of the listed company

Note:

- The total number of issued and paid-up shares of the company prior to the share issuance for asset payment shall be used.

- The total number of issued and paid-up shares of the company prior to the share issuance for asset payment shall be used.

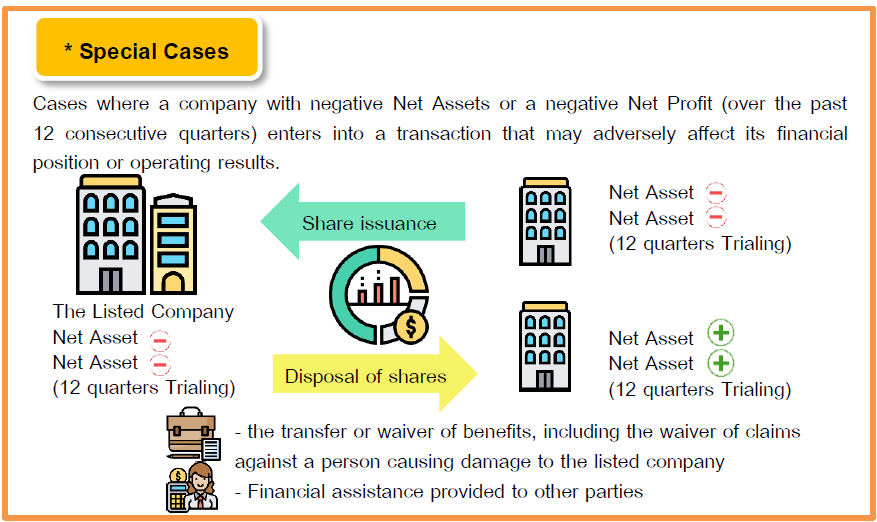

Special Cases

- Material Transaction in Special Cases refers to cases where a company has negative Net Assets (NA) or has incurred a Net Loss (considering the operating results of the past 12 consecutive quarters), and enters into a transaction that may adversely affect the company's financial position or operating results.

- Material Transaction in Special Cases refers to cases where a company has negative Net Assets (NA) or has incurred a Net Loss (considering the operating results of the past 12 consecutive quarters), and enters into a transaction that may adversely affect the company's financial position or operating results.

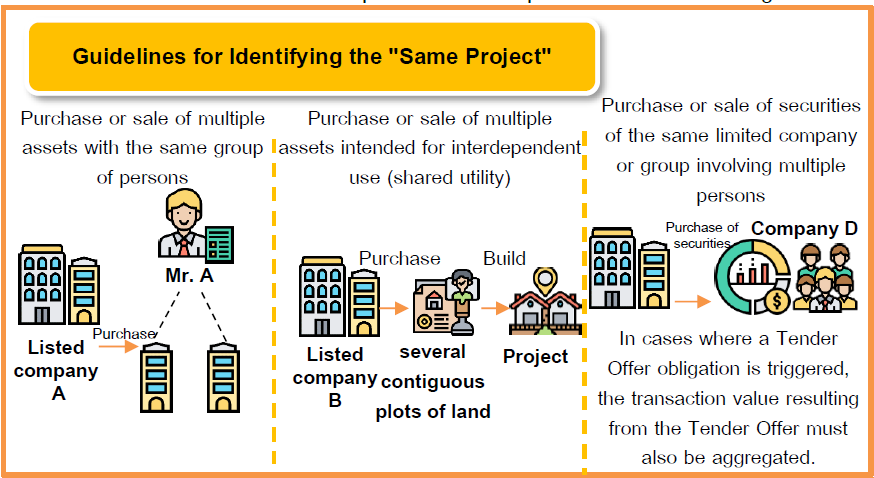

Aggregation of transaction size

- The calculation of the transaction size must include related transactions or transactions under the same project occurring during the 12 months prior to the date of agreement to enter into the transaction (the date on which the Board of Directors passes a resolution to approve the transaction), except for transactions that have already received shareholder approval.

In this regard, the SEC has the authority to aggregate multiple transactions into a single transaction if the facts indicate that the company intended to split the transactions to circumvent compliance with the prescribed rules and regulations

- The calculation of the transaction size must include related transactions or transactions under the same project occurring during the 12 months prior to the date of agreement to enter into the transaction (the date on which the Board of Directors passes a resolution to approve the transaction), except for transactions that have already received shareholder approval.

In this regard, the SEC has the authority to aggregate multiple transactions into a single transaction if the facts indicate that the company intended to split the transactions to circumvent compliance with the prescribed rules and regulations

Aggregation of transaction size

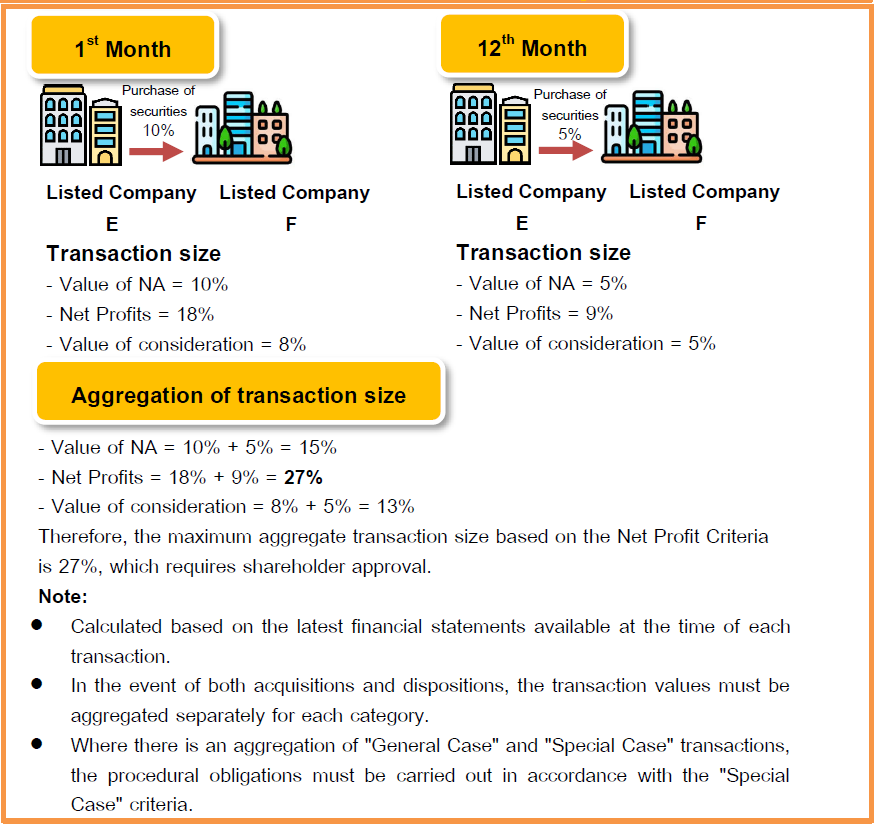

- Value of NA = 10% + 5% = 15%

- Net Profits = 18% + 9% = 27%

- Value of consideration = 8% + 5% = 13%

Therefore, the maximum aggregate transaction size based on the Net Profit Criteria

is 27%, which requires shareholder approval.

Note:

• Calculated based on the latest financial statements available at the time of each transaction.

• In the event of both acquisitions and dispositions, the transaction values must be aggregated separately for each category.

• Where there is an aggregation of "General Case" and "Special Case" transactions, the procedural obligations must be carried out in accordance with the "Special Case" criteria.

- Value of NA = 10% + 5% = 15%

- Net Profits = 18% + 9% = 27%

- Value of consideration = 8% + 5% = 13%

Therefore, the maximum aggregate transaction size based on the Net Profit Criteria

is 27%, which requires shareholder approval.

Note:

• Calculated based on the latest financial statements available at the time of each transaction.

• In the event of both acquisitions and dispositions, the transaction values must be aggregated separately for each category.

• Where there is an aggregation of "General Case" and "Special Case" transactions, the procedural obligations must be carried out in accordance with the "Special Case" criteria.

Procedures upon the size of transactions |

- After calculating from all different bases, choose the highest value to proceed

- Summary of the process according to the calculated transaction size:

- Summary of the process according to the calculated transaction size:

| Transaction size | Procedure | ||||

| General Case | Special Case | BOD + Disclose information | Shareholder approva | IFA | Progress Report |

| X < 25% | X < 10% | - | - | - | - |

| 25% ≤ X < 50% | 10% ≤ X < 25% | - | |||

| X ≥ 50% | X ≥ 25% | ||||

| X ≥ 100% (Backdoor Listing) | + Relisting Submission | ||||

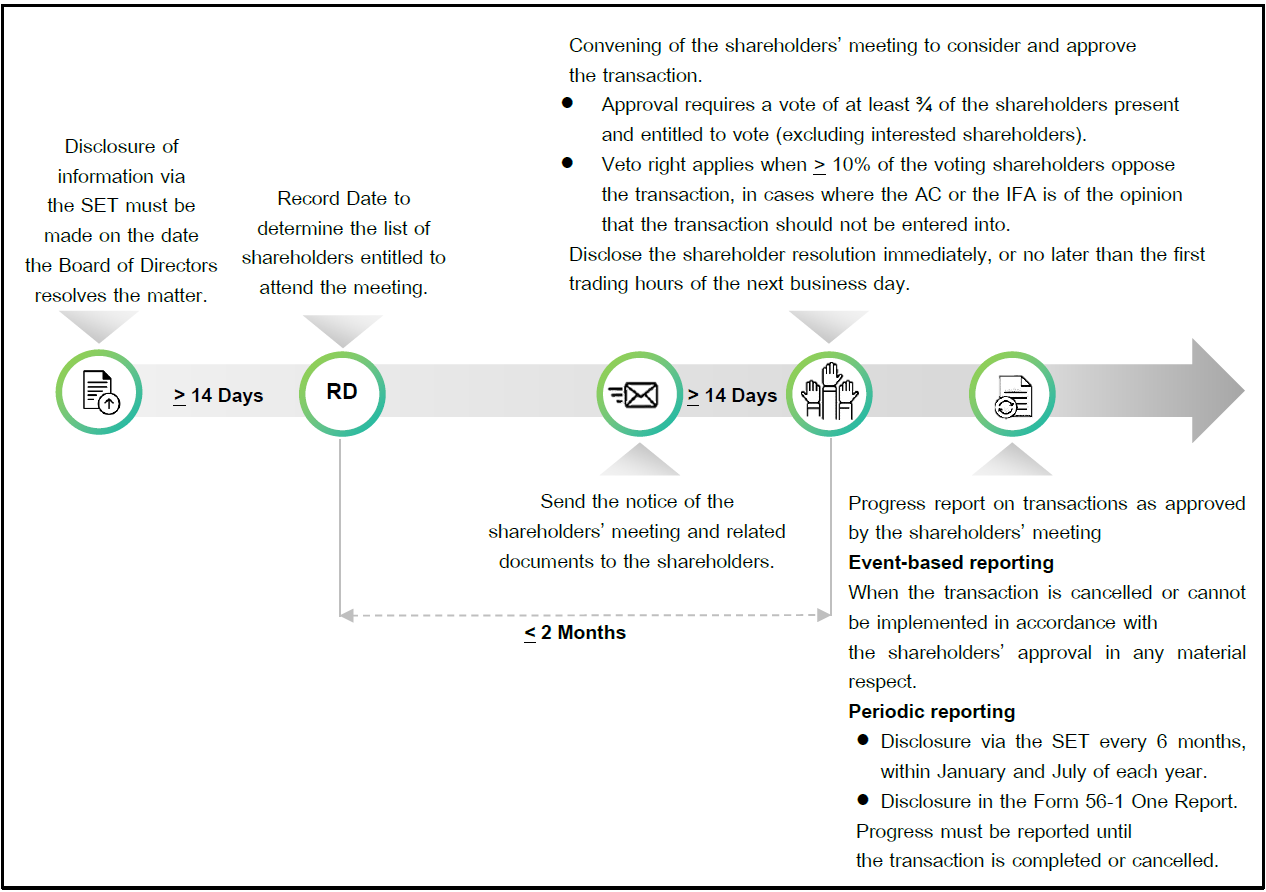

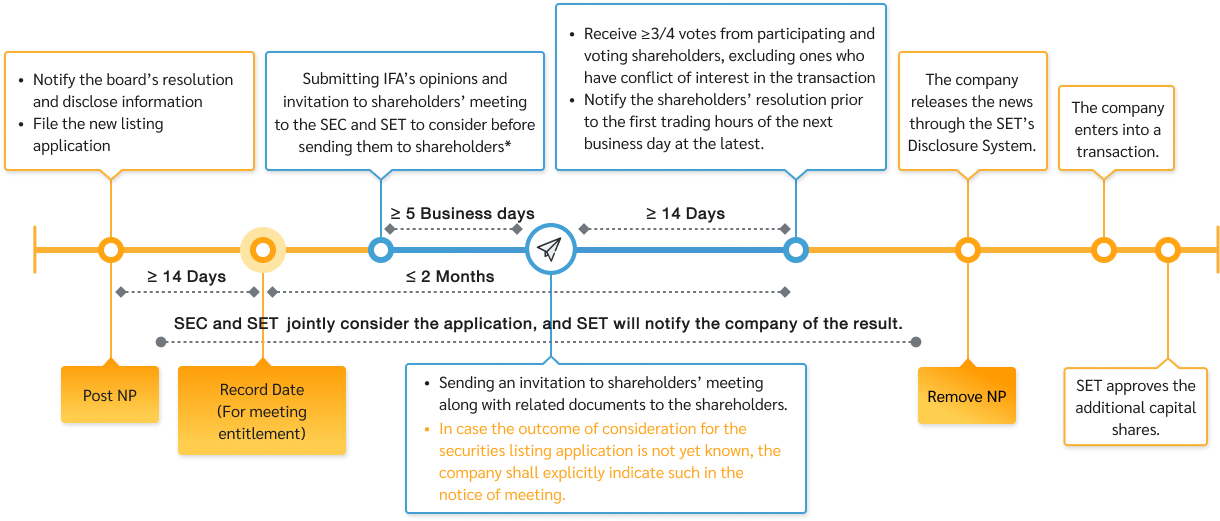

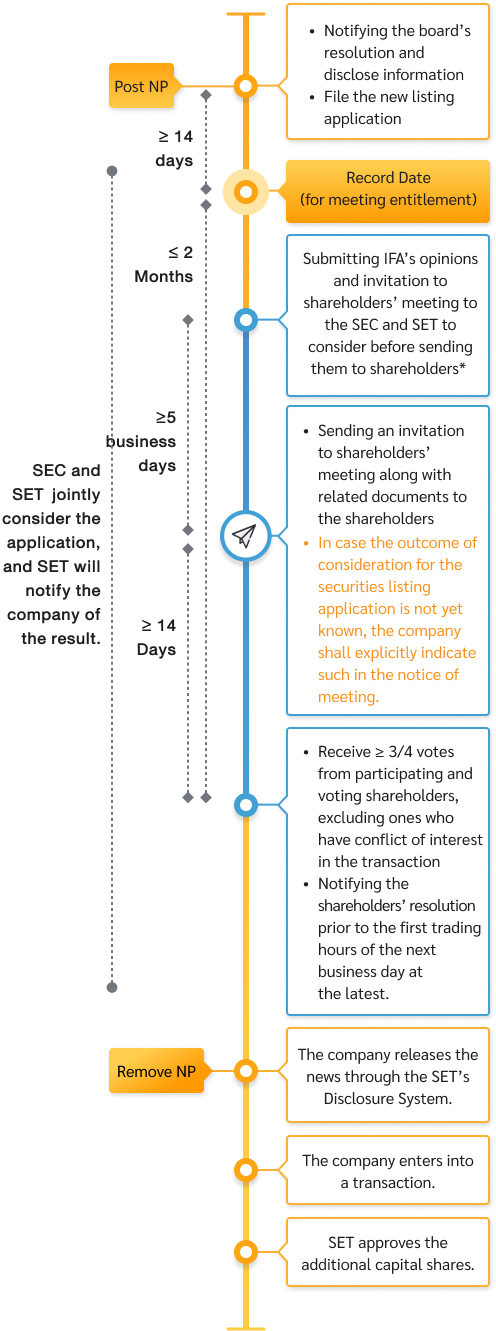

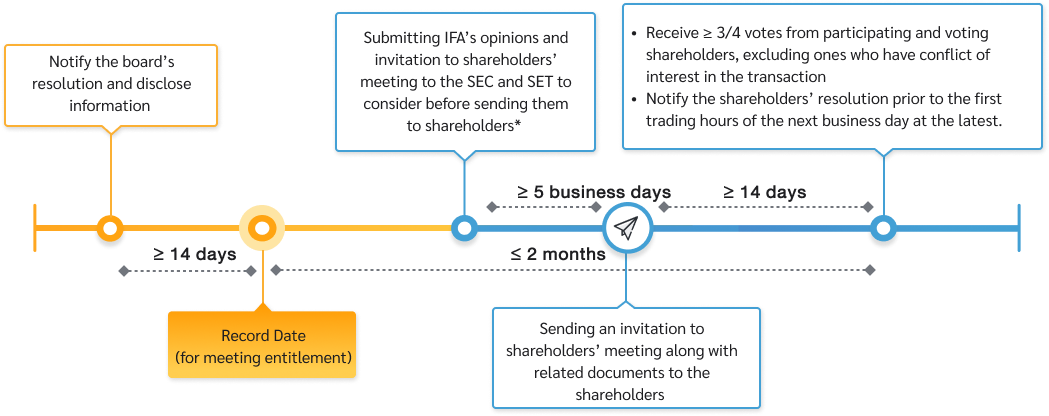

The transaction must be approved by the shareholders' meeting with a vote of not less than ¾ of the total number of votes of the shareholders attending the meeting and having the right to vote, excluding the votes of shareholders with a conflict of interest.

Veto Rights

If IFA or AC is of the opinion that the transaction should not be entered into, shareholders holding an aggregate of more than 10% of the total votes of the shareholders attending the meeting and having the right to vote may cast a vote to object to and block the transaction.

If IFA or AC is of the opinion that the transaction should not be entered into, shareholders holding an aggregate of more than 10% of the total votes of the shareholders attending the meeting and having the right to vote may cast a vote to object to and block the transaction.

Exemption of Obligations for Transactions Conducted by a Listed Subsidiary |

- Exemptions from duties within the company, and cases where a subsidiary is a listed company.

The company shall be exempt from the obligations under the material transaction criteria for any transaction undertaken by its listed subsidiary. (The subsidiary shall be the sole party responsible for complying with the regulations governing material transactions arising from such transaction.)

- Exemption of obligations in cases where prior disclosure or seeking prior shareholder approval may significantly prejudice the interests of the company or its subsidiary.

In the event that the company faces constraints in complying with the regulations governing material transactions (such as participating in an auction or a competitive bidding process, which may involve certain terms or conditions that prevent the disclosure of transaction details, or where disclosing certain information could place the company at a competitive disadvantage), and the Board of Directors has considered with responsibility, due care, and loyalty in accordance with their fiduciary duty that if the company is required to disclose information prior to entering into the transaction or to obtain prior approval from the shareholders' meeting by disclosing the minimum required details as prescribed in the regulations, it could cause significant damage to the benefits of the listed company or its subsidiaries; the listed company may proceed in accordance with the following guidelines:

(1) Seek prior approval from the shareholders' meeting for a framework and principle, authorizing the Board of Directors to proceed as appropriate within such approved framework.

(2) Disclosure of information shall be at the discretion of the Board of Directors, taking into account the potential benefits and impacts on the company.

In this regard, the company shall be exempt from the requirements regarding prior disclosure (Transaction Information Memorandum) and the minimum information requirements for seeking approval (Notice of Meeting and Independent Financial Advisor’s Report).

(3) The company has to disclose the transaction information via the Stock Exchange’s electronic system after the agreement to enter into the transaction has been reached, by applying the minimum disclosure requirements mutatis mutandis.

The company shall be exempt from the obligations under the material transaction criteria for any transaction undertaken by its listed subsidiary. (The subsidiary shall be the sole party responsible for complying with the regulations governing material transactions arising from such transaction.)

- Exemption of obligations in cases where prior disclosure or seeking prior shareholder approval may significantly prejudice the interests of the company or its subsidiary.

In the event that the company faces constraints in complying with the regulations governing material transactions (such as participating in an auction or a competitive bidding process, which may involve certain terms or conditions that prevent the disclosure of transaction details, or where disclosing certain information could place the company at a competitive disadvantage), and the Board of Directors has considered with responsibility, due care, and loyalty in accordance with their fiduciary duty that if the company is required to disclose information prior to entering into the transaction or to obtain prior approval from the shareholders' meeting by disclosing the minimum required details as prescribed in the regulations, it could cause significant damage to the benefits of the listed company or its subsidiaries; the listed company may proceed in accordance with the following guidelines:

(1) Seek prior approval from the shareholders' meeting for a framework and principle, authorizing the Board of Directors to proceed as appropriate within such approved framework.

(2) Disclosure of information shall be at the discretion of the Board of Directors, taking into account the potential benefits and impacts on the company.

In this regard, the company shall be exempt from the requirements regarding prior disclosure (Transaction Information Memorandum) and the minimum information requirements for seeking approval (Notice of Meeting and Independent Financial Advisor’s Report).

(3) The company has to disclose the transaction information via the Stock Exchange’s electronic system after the agreement to enter into the transaction has been reached, by applying the minimum disclosure requirements mutatis mutandis.

Information disclosure |

- The company must disclose the Board of Directors' resolution regarding a significant transaction immediately upon the agreement to enter into the transaction. This disclosure must be made within the day of the Board's resolution or, at the latest, prior to the first trading session of the next business day via the SETLink system.

- Information disclosure must comply with the guidelines prescribed by SEC. Key information required in the Board's resolution includes:

1) At least the following details must be disclosed:

1.1) The date or the expected timeframe for the transaction.

1.2) Names of the parties involved and their relationship with the listed company or its subsidiaries. In the case of a related party transaction, specify the relationship that qualifies them as related persons.

1.3) Details such as a summary overview, objectives, procedures, and conditions of the transaction.

1.4) Asset details must include the type and current condition of the asset, along with any existing debts or legal encumbrances. In the case of securities, general business information is required, such as the nature of the business, registered and paid-up capital, and a summary of financial health and earnings over the past 3 years. Additionally, the disclosure must list the Board of Directors and the top 10 shareholders with their ownership percentages, clearly identifying the ultimate shareholders (actual owners). If any persons related to the company also hold shares in that business, their names and ownership stakes must be specifically disclosed.

1.5) Total transaction value and payment methods, including conditions such as payment schedule, installments, or deposits. If the consideration is non-cash (e.g., issuance of securities or asset exchange), specify the type and details of such assets/securities and the valuation methodology.

1.6) For the transaction size calculation, must provide the following details:

- The calculation results based on the 4 criteria. If any criterion is not applicable, the reason must be stated.

- The maximum calculated transaction size and the resulting obligations the company must fulfill.

1.7) Source of Funds/Plan for Use of Proceeds. If funded by loans from financial institutions, specify conditions that may affect shareholder rights, such as dividend payment restrictions.

1.8) In cases of investing in an entity where connected persons hold more than 10% of the total voting shares, and such entity becomes an associate or subsidiary after the transaction, the company must explain why this shareholding structure is in its best interest. Additionally, the company must specify measures to prevent any potential conflicts of interest that may arise in the future.

1.9) Reports from independent experts, such as asset appraisers or financial advisors (if any).

1.10) Key terms and conditions of relevant agreements.

1.11) If the transaction requires approval from relevant regulatory authorities, details must be disclosed, such as the names of the regulators, the applicable laws, the conditions for approval, and the expected timeframe for the application process.

1.12) Litigation related to the transaction or the assets involved (if any).

1.13) Other data that may significantly impact investors' decisions.

2) Business Plan related to the Transaction

2.1) Business policies and operational plans related to the transaction, specifying a brief timeframe.

2.2) Analysis of market conditions and competition, including business opportunities.

2.3) Risk factors or events that may impact the ability to execute the plan as intended.

2.4) Contingency plan in case the transaction cannot be successfully completed, including an analysis of potential impacts.

Note: Information in categories that are inconsistent with the nature of the transaction may not be disclosed. For example, in the case of receiving financial assistance from a related person to resolve liquidity issues or for use as working capital, it may not be necessary to disclose information regarding market conditions and competition, including business opportunities.

3) Opinion of the Board of Directors on at least the following matters:

3.1) Reasonableness and benefits of the transaction.

3.2) Potential risks or impacts arising from the transaction.

3.3) Suitability of the price and transaction conditions.

4) The Board’s certification stating that they have reviewed the information with due care and consider the transaction to be reasonable and for the benefit of the company and shareholders.

5) Opinion of the Audit Committee

6) Certification that interested directors in a related party transaction did not attend the meeting and did not vote in the Board of Directors' meeting to approve such transaction (Specific to related party transactions).

Opinion of the Independent Financial Advisor (IFA) |

- A brief summary of the transaction overview. In this regard, reference may be made to the details disclosed by the Company in the notice of the shareholders’ meeting.

- The opinion of the independent financial advisor, including an explanation of the supporting reasons and key assumptions on at least the following matters:

- - The reasonableness of and benefits from the transaction

- The risks or potential impacts arising from the transaction

- The appropriateness of the transaction price and conditions

- - The reasonableness of and benefits from the transaction

- A summary of the independent financial advisor’s opinion as to whether the shareholders should approve the transaction, together with supporting reasons.

- A certification of performance confirming that the duties have been performed with due care, prudence, and in accordance with professional standards, with primary regard to the interests of the Company’s shareholders.

Notice Convening the Shareholders’ Meeting |

- Dispatch the notice of the shareholders' meeting to shareholders at least 14 days prior to the meeting date, and simultaneously disclose the notice via the SETLink system, which must include the following minimum required disclosures :

- Minimum items required to be disclosed in the information memorandum relating to the transaction (as disclosed through the SET).

- Specify the names and number of shares held by interested shareholders who are not entitled to vote.

- A proxy form allowing shareholders to cast votes at their discretion, together with the nomination of at least one audit committee member to act as proxy for shareholders.

- In the event that the audit committee or the financial advisor is of the opinion that the shareholders should not approve the transaction, the rights of shareholders to object to the transaction must also be specified.

- The Independent Financial Advisor’s (IFA) opinion report (applicable to transactions whose size triggers the compilation requirement).

Progress reporting (Shareholder-approved transactions only) |

A listed company is required to report the progress of the transaction through the Stock Exchange of Thailand’s electronic disclosure system (SETLink), as prescribed by the SEC, only for transactions that have been approved by the shareholders.

- Event-based reporting: The company must report immediately within the next business day from the date on which it knew or should have known of such event when:

- the transaction is cancelled; or

- the company is unable to proceed with the transaction as approved by the shareholders in any material respect, such as changes to the transaction timeline, transaction conditions, counterparties, transaction value, etc.

- Reporting must continue until the transaction is completed or cancelled.

Reporting schedule and disclosure channels

| Reporting period | Reporting timeline | Disclosure channel |

| 1) 6-month reporting period | By 31 January and 31 July of each year | Disclose information via the SETLink system |

| 2) 1-year reporting period | Within 3 months from the end of each fiscal year-end period | Form 56-1 One report |

Information to be Disclosed

| Transaction | Type of Transaction | Date of approval | Summary of the transaction | Progress status | |

| Transaction sequence | Specify transactions that are: Note: For transactions that have been completed or cancelled during the current reporting period, the company is not required to continue reporting their progress in subsequent reporting periods. | Specify whether the transaction is a material transaction, a related party transaction, or falls under both categories. | Specify the date of approval from the shareholders’ meeting. | Provide a brief summary of the transaction as approved by the shareholders’ meeting. | - Specify the latest progress status as of the present date. |

Process

Related Regulations

|

|

|

|